Guaranteed Universal Life Insurance, The Ultimate Guide

It’s never too early or too late to choose a good life insurance policy. However, some insurance policies can be daunting because of their monthly premium alone. Others may come at an affordable price but may not pay out the death benefit you are looking for if you were to outlive the coverage. That’s why Guaranteed Universal Life Insurance is great because it offers a middle ground between both term life and whole life insurance.

Guaranteed Universal Life Insurance can be a great fit for anyone at any age. It has a number of benefits that solve an array of issues like being to able to provide your family with money to pay off unpaid debts or replace an income stream. It can also be used to leave a legacy to kids, grandkids charities, and more.

Let’s get into what GUL is and why it could be your best solution when it comes to getting life insurance.

What Is Guaranteed Universal Life Insurance?

Guaranteed Universal Life Insurance is permanent life insurance that is generally considered to be a cross between term life insurance and whole life insurance. This is because you can pay a fixed rate for the desired term length while also being guaranteed the death benefit. The rates are much more affordable than whole life because GUL doesn’t have all the frills that whole life has.

A major difference is that although there may be minimal cash value that builds up within a GUL policy, it’s just that…very minimal. This is by design. The idea is you are just paying the minimum that’s required to guarantee the policy stay in force. Instead of extra money going into the policy which could increase the cash value instead you get to keep that money in your pocket.

Benefits and Drawbacks

Like any life insurance, you are going to have the parts that are appealing and the parts that make you think twice. While GUL typically offers the well-rounded best-of-everything option, it is not perfect.

These are also general pros and cons. Each insurance company may offer something different within their own specific policies.

Pros of Using GUL Policies

There are tons of positives to choosing a Guaranteed Universal Life Insurance plan. They include but are not limited to the following.

- Permanent Coverage at an Affordable Rate

- Guaranteed Death Benefit Amount

- Flexibility to Decrease the Benefit

- Potential Return of Premium

Lifelong Coverage for Less

It is unlikely that you will find a better deal than GUL for lifelong life insurance coverage because you don’t have to pay the expensive premiums that come with whole life insurance. As mentioned, this is because you are not paying for the extra frills and add-ons that come with whole life insurance. Essentially you can cut the fat out.

While this is a great option for seniors looking to start a policy, it is also a great option for those who are just starting out and don’t want to put their money into term life insurance.

The Guaranteed Death Benefit Amount

Some people don’t like going with term life policies because it is sort of like renting an apartment. You never see that money again. It’s just designed to cover you until you can potentially find a more permanent solution.

When you go with GUL policy you are putting money into your policy knowing that a some point the death benefit will be paid out to your beneficiaries no matter what! Of course this is because we will all pass away eventually. This is an important consideration when picking a life insurance option, and it’s usually the reason why people find themselves going with the middle option (GUL).

Ability To Decrease The Benefit

A major pro in choosing this type of life insurance policy is the ability to make changes on the fly. The truth is your needs are going to be very different at 40-years-old than they will be at 70-years-old. If you are 40 and have to worry about not only covering a mortgage but also your children’s tuition for school, a death benefit that covers this makes sense.

However, when you get older than 60-years-old and have possibly paid all this off, you may not need this amount of coverage anymore. That’s why decreasing the death benefit is a great option to lower your premiums as you get older and have the ability to change with your needs.

Return Of Premium

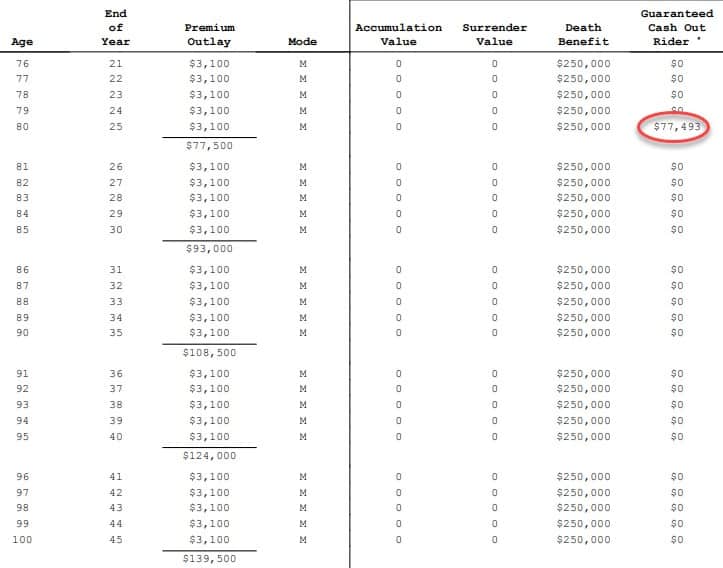

Some GUL policies will even offer a return of premium feature on the policy. For example, below is a an example with one insurance company. The example is on a 55 year woman with a death benefit of $250,000. The monthly premium is $258.31 which is $3,099.72 per year. In the example below you will see it actually shows $3,100, because it is rounding up the 28 cents to a full $3,100.

On this specific policy in year 15, 20, and 25 there is a 60 day window where if someone wants to cancel the policy they can do so and receive a guarantee return of premium of the amount indicated. For this 55 year old woman the way it works is she should cancel the policy in year 15 and get $30,222 returned back to her. That’s 65% of the total premiums she paid. Alternatively, if she were to cancel in year 20 or 25 within the respective 60 day window they would return 100% of the premium that she paid in.

To be clear if she took this money the policy would be canceled. However, sometimes the need or desire for coverage changes. If so, this offers some flexibility in the future for her to get back what she paid in at these specific times. If she does not take the refund in year 25 then as long as she continues to pay the premium the policy will stay in force for the rest of her life. When she eventually passes away the $250,000 death benefit would be paid to her beneficiaries.

Drawbacks of Using GUL Policies

Policies aren’t perfect and here is where some users draw concern about GUL’s. While these may be negative to some, some customers actually see things like no cash value as a positive.

- No Cash Value (or little cash value and some like the example above do have return of premium premium features.

- Strict Payment Policy

- Medical Exam

No Cash Value

While Guaranteed Universal Life insurance policies are incredibly stable, they aren’t designed to build up cash value at all. Because of this, there is minimal cash value accrual. Essentially you are getting what you put into your policy and no more than that.

Some permanent life insurance policies other than GUL add a huge cash component to their policies. But with that may ome the risk that your policy could lapse depending on the type of policy you are purchasing. A whole life policy would stay in force for life as long as the premium is paid. The drawback again is the much higher premium.

Strict Payment Policy

Something that really sets GUL policies apart from some others is that you don’t have any flexibility or wiggle room for when your payments are due. You must pay on-time or risk the policy being terminated or shortening your policy in general.

Other policies have a little more room for flexibility and may allow you to miss payments with opportunities to make up the payments down the road.

Medical Exams

Some life insurance policies will allow you to skip a medical exam as a part of your application. As a part of the application process for Guaranteed Universal Life Insurance you may or may not have to complete a medical exam. It depends on the insurance company that you apply with.

While this may be a little inconvenient if you have to do an exam, these exams really aren’t that much of a hassle. Instead of having to make a trip to the doctor’s office, the insurance company will actually send an examiner to your home at a convenient time for you. The exam itself usually takes no more than 20-30 minutes.

You may even be able to get a better rate after completing an exam if you are in exceptionally good health.

Who Is GUL Aimed At?

GUL is a great fit for many people because of its benefits and affordability. Some of the reasons you may wish to own a GUL include if you:

- Have a dependent with special needs (Spouse/Child/Family)

- Own a business

- Have a larger debt

- Are concerned about Estate tax protection

- Desire to leave an inheritance

- Have a term policy that’s coming to the end of it’s level term period.

Making sure that your beneficiaries don’t take on your debt or being able to care for your loved ones after passing are the main forms of needing life insurance. Also protecting your estate and leaving an inheritance that you don’t want creditors to come after is a popular reason.

GUL insurance policies are just as important for someone who is 40 as it for someone who is 70 and needs life insurance. Most people need it, it’s why they need it and how much they need that determine the coverage amount and specific policy design.

In order to get the benefits of the lower-cost premiums, don’t forget that the earlier you start the lower your monthly premiums will be.

So, if you are 70 and just starting a new policy, you may be paying more than someone who is 80 that had started their policy and locked in their rates at 60-years-of-age.

Top Companies Who Offer GUL

These are some of the top companies that currently offer GUL policies that have been widely-used and highly rated by customers of all ages.

American National

American National is based out of Springfield, Mo and has been around since 1905. Consistently a top contender when it comes to GUL insurance. They offer their Signature Guaranteed UL with several important features.

You can expect:

- Small coverage amounts available – as low as $25,000

- They also allow you to customize your policy and choose your preferred guarantee period

- Ability to cancel your policy and cash out at certain times periods.

- Living benefit riders including chronic, critical, and terminal illness.

Symetra

Symetra is based out of Des Moines, IA and has been around for over 60 years. They offer their UL-G and have been competitive in pricing for quite some time. They have a lot of interesting features that customers with specific needs have capitalized on.

You can expect:

- Coverage amounts starting at $100,000

- Offers a chronic illness rider that allows early access of up to half of the death benefit while you are alive.

- The ability for return of premium on the rider.

- Plenty of rider options.

North American

North American is based out of Sioux Falls, SD and has been around since 1886. They have high financial ratings and rate extremely high in stability and have served many satisfied customers.

You can expect:

- Allows for the length of the coverage to be guaranteed until 120-years-of-age.

- Ability to switch your GUL for any of North American’s Universal Life Insurance products.

- Focus on protecting the next generation.

Protective Life

Protective Life has been in the business for over 110 years which means they know exactly what they are doing. Their GUL products are some of the strongest offered in the market and their assets can back this up.

Their products products include the Life Assurance Protector GUL, Advantage Choice UL, and the Custom Choice UL.

You can expect:

- Great affordable coverage.

- Customizable options like being able to guaranteed the coverage for a shorter period of time if desired to save money.

- Optional Extend Care rider to provide access to your death benefit while you’re alive to help pay for chronic illness costs. (extra fee for this optional rider)

GUL Verse Whole Life

While we know the GUL serves as the middle-man between all the life insurance policies there are some notable differences between Guaranteed Universal Life Insurance and Whole Life Insurance that should be talked about when choosing one or the other.

Similarities

The most important thing to know is that both of the policies have a guaranteed death benefit because they are both considered to be permanent life insurances. They both can be great options for providing protection for a spouse. For instance if one spouse passes away a Social Security check stop. Life insurance can help replace what Social Security would have provide. It can also be a good way to leave a legacy, provide liquidity to help pay for possible income or estate taxes, and to make sure any unpaid debts aren’t passed down to the next generation.

Differences

But they do have a number of differences that are worth talking about. Here’s the two key differences though:

- Your price point is going to be the first noticeable difference. Whole Life Insurance is a lot more expensive than GUL.

- Cash value is the next thing. GUL really accumulates no cash value where Whole Life builds up cash value over time.

In simple terms, Whole Life insurance is kind of like a GUL with a savings vehicle built-in.

Shop Around

Even with knowing all this information about GUL policies, it is best to start by shopping around. The first company may sell you something that sounds great but each insurance company will have special features that make their policies unique. What is also important to consider is going through an independent agency.

Reading through the information firsthand is beneficial but there are a lot more complications that can overwhelm a customer. Using an independent agency that is impartial to the process can really help you narrow down a company and policy that fit your needs. That way if an insurance company has left out valuable information about a policy that could affect your goals, an independent agency can quickly pick up on this.

Remember, Guaranteed Universal Life Insurance is not for everyone. Everyone’s needs are different and the key is making sure you get the best plan for your particular situation.